- Are Financial institutions now Legalized "Loan sharks?"

- Are credit cards a trap?

- Are unsecured credit cards really unsecured?

- Is your money really under your control in a bank or a credit union?

- Is there a code of ethics associated with the banks and credit unions' debt collection process?

- Isn't it easier for banks and credit unions to maintain "fake accounts" versus retain "real accounts?"

Legalized "Loan Shark" Coastal Federal Credit Union instructed the sheriff to:

" . . . do hereby levy upon Any and all accounts and or assets found at your institution up to, but not to exceed $44,171.01."

Principal: $20,921.23

Interest: $18,252.06

Court Cost: $ 3,908.18

Other Cost: $ 1029.54

Total DUE: $44,171.01

Nine years of compounding interest and fees can really add up

on an unsecured CREDIT CARD in default!

So Coastal Federal Credit Union attorneys "coincidently" levies on my business banking account at the beginining of the month just before my mortgage check is scheduled to clear. BB&T Bank repeatedly returns the mortgage check even though my posted balance is high enough to clear the mortgage.

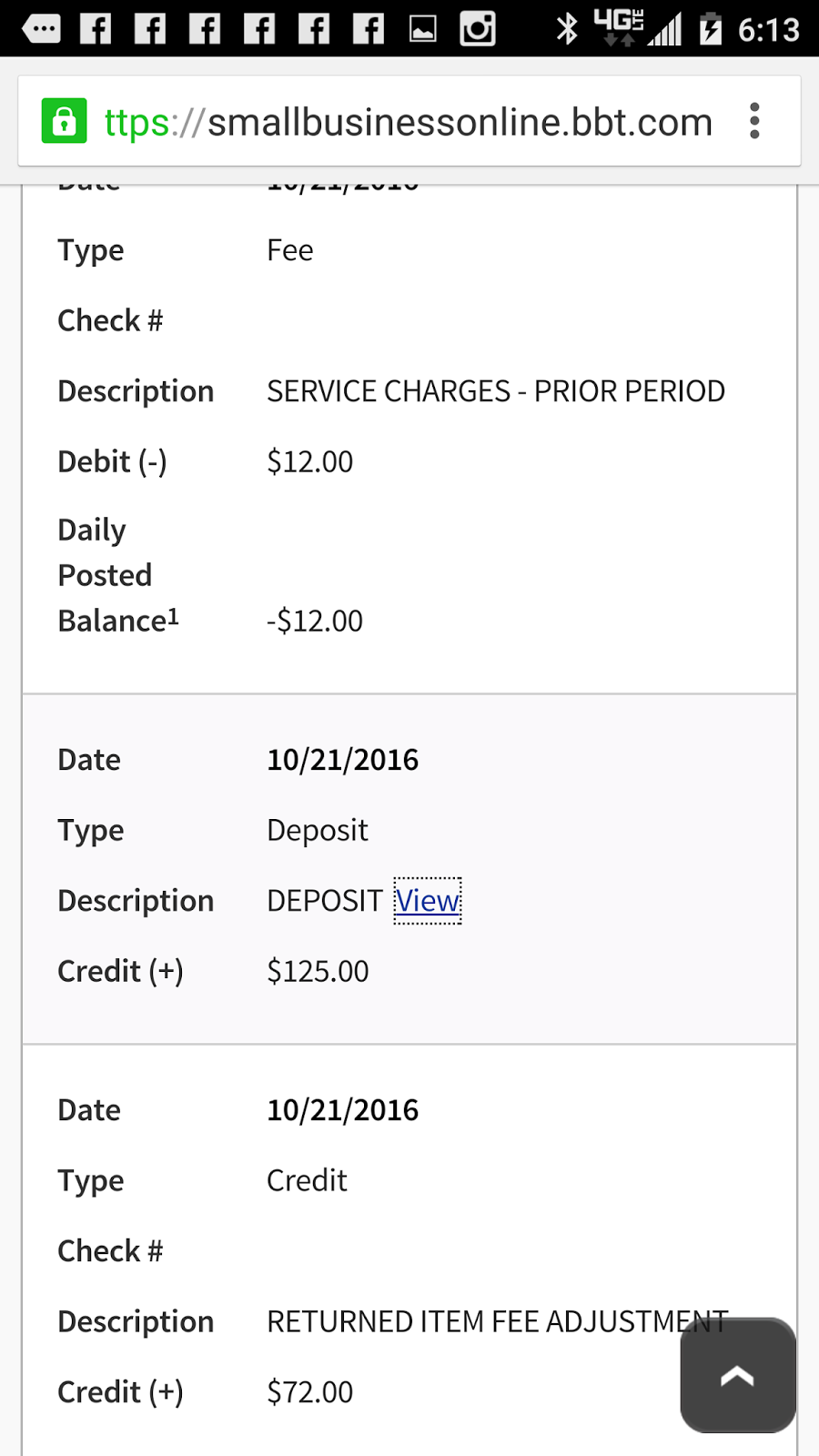

Notice that the Administrative Hold is for $44,296.01? Well, BB&T Bank charges $125.00 to extort me out of all of my money. So $44,171.01 + $125.00 = $44,296.01

I have been an accountholder with Branch Banking and Trust Company (BB&T) Bank for over a decade. I would have appreciated a phone call or at least, received a notice in my online banking inbox about the levy against my account.

However, as you can see, BB&T did NOT attempt to personally notify me through my online banking inbox of the Coastal Federal Credit Union's levy against my business banking account. My last inbox message from BB and T Bank was from March 2016.

Actually, BB&T Bank just casually dropped me a letter in the US Postal Mail. It was NOT certified, and it was delayed in arriving to me.

The Branch Banking and Trust Company letter essentially says that

- We are taking all your money out of your account.

- We are taking all additional deposits that you make to your account.

- We are charging you a non-refundable fee of $125.00 onto your account

- and call us if we can be of further assistance!

With this kind of customer service surrounding "real accounts," I hope that BB&T doesn't have any "fake accounts."

So what type of customer was I? My business account was very dynamic. It had its "highs and lows."

For instance, I was two cents ($.02) SHORT, and BB&T charged me a $36.00 overdraft fee. I did not even complain. I did not even ask for a credit nor refund.

Notice my posted balance is negative $36.02? I was two cents short plus short their $36.00 overdraft fee for a total of -$36.02. This is how BB&T bank does business.

Also, notice my posted balance on 10/7/2016 was $1,989.35 while my posted balance on 10/5/2016 was $1,474.35. So again, my business account was revolving with deposits and withdraws.

So now, my account has been levied for $2,114.35 which is MORE than my posted balance.

And my new BB&T account balance is still in the negative. -$197.00

Well, that's better than the -$42K!!!

Is this all legal? I am asking the Consumer Finance Protection Bureau (CFPB) and the National Credit Union Administration (NCUA) each this very question.

These "loan sharks" ( I mean) bank and credit union seem to be more ruthless the Internal Revenue Service (IRS). At least, the IRS never takes one's last dime. They leave a little money for people to live with. Why don't banks and credit unions follow the same courtesy or rules?